2026 1st quarter investment bulletin

Executive Summary

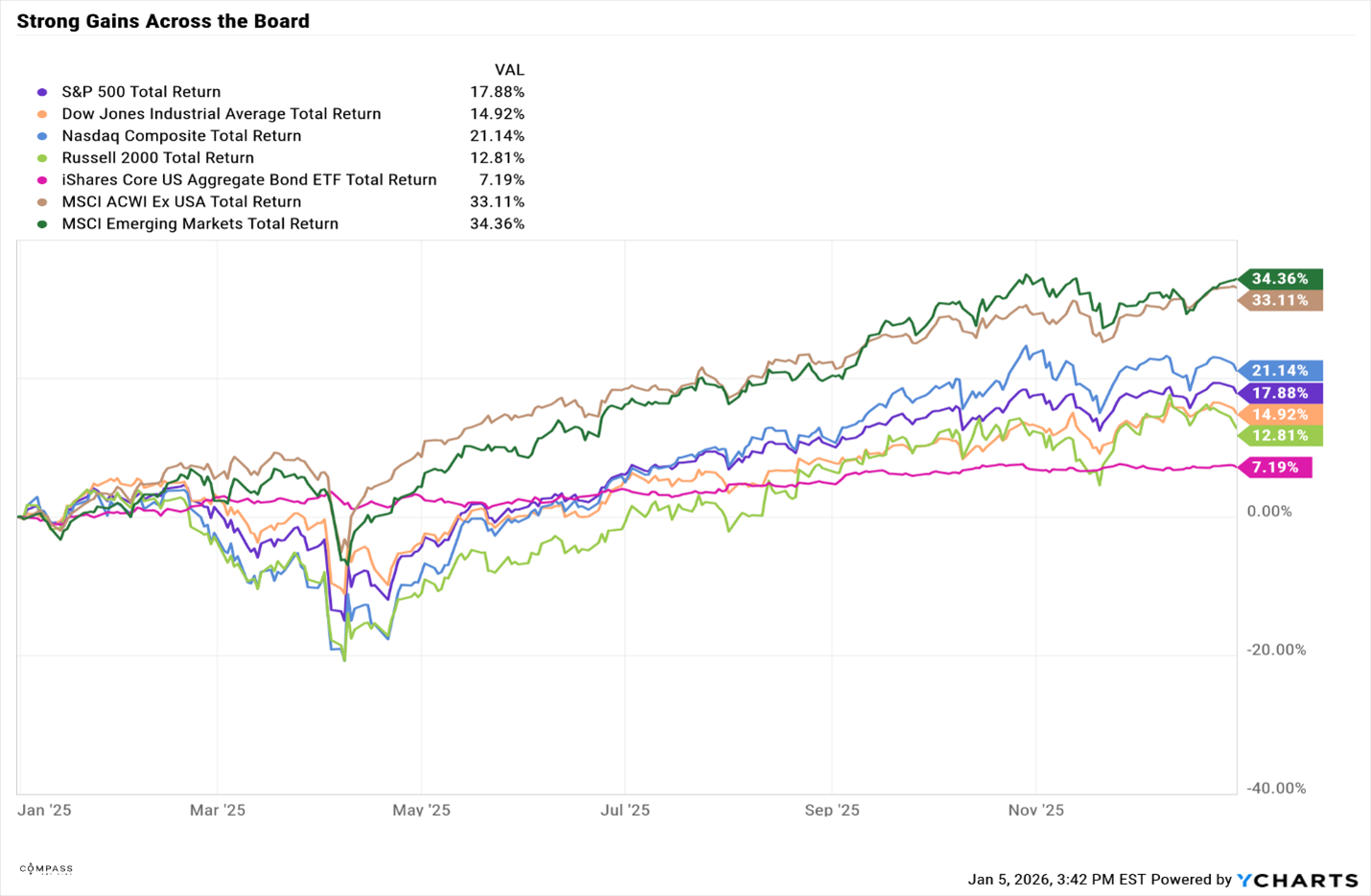

Despite stumbling early in 2025, stocks achieved double-digit gains for the third year in a row. The technology sector continued to be a winner in the U.S. However, overall total performance was led by international stocks.

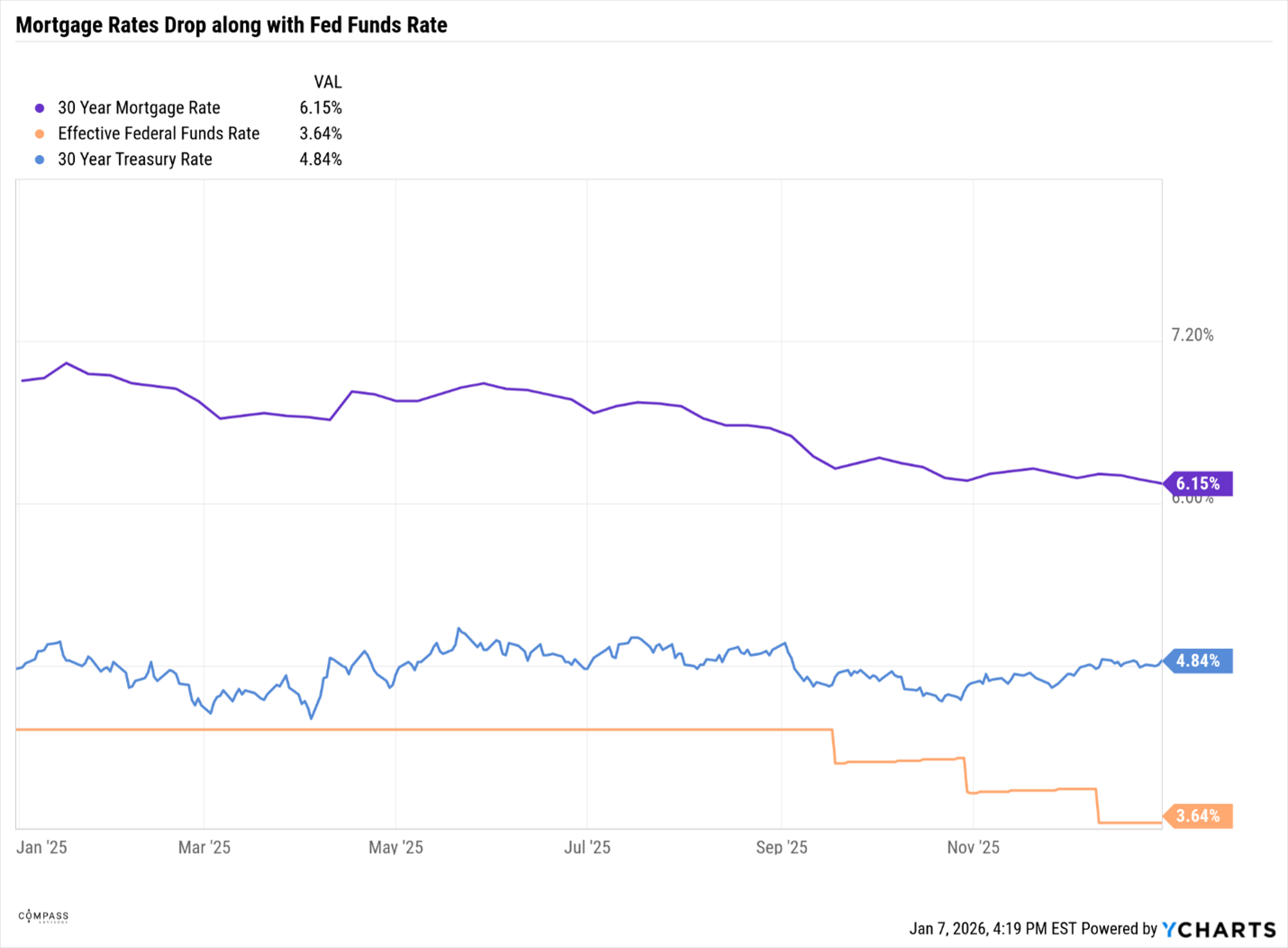

Bonds benefited from a Federal Reserve that cut rates three times during the year.

The economy has remained strong as evidenced by a material rebound in Gross Domestic Product (GDP).

Inflation remains higher than the Fed’s target but has been continually moving lower in the last few years.

U.S. Stocks Powered by Tech Leaders in 2025

U.S. stocks finished 2025 with broad double‑digit gains, marking a third consecutive bullish year for large‑cap equities. Performance remained highly concentrated, with technology and AI‑linked names driving the Nasdaq 100 to another year of outperformance and helping push the major indices to or near record highs.

Stock prices rose primarily because companies earned more money (not just because investors were willing to pay higher premiums), with mega-tech and financial companies leading the way. However, performance varied widely across sectors, making selectivity important. Notably, international equities advanced strongly, with the MSCI All Country World ex‑USA index gaining 33.11% for the year.

Rates Fall, but Housing Remains Stuck

The Federal Reserve's three 0.25% rate cuts marked a meaningful shift in 2025 from “higher for longer” to a more gradual easing cycle. Treasury yields drifted lower throughout the year, with the benchmark 10-year rate lingering most of its time between 4% and 5% before settling near the low by December. For bond investors, this translated into welcome relief. High quality fixed income delivered positive total returns after a bruising stretch when rising rates hammered principal values in 2024.

Housing told a more complicated story. Mortgage rates did fall, the average 30-year fixed rate dropped from 6.91% to 6.15% over the course of the year, but that hardly triggered a surge in activity. Home prices actually climbed about $7,400, or 1.7%, to a new median high, proving that elevated rates do not necessarily make homes cheaper; they just freeze the market.

Affordability remains a stubborn challenge. For households considering a move or downsizing, careful timing and creative financing strategies may help as rates inch lower but stay well above pre-pandemic levels.

Tariffs, Geopolitics, and Simmering Tensions

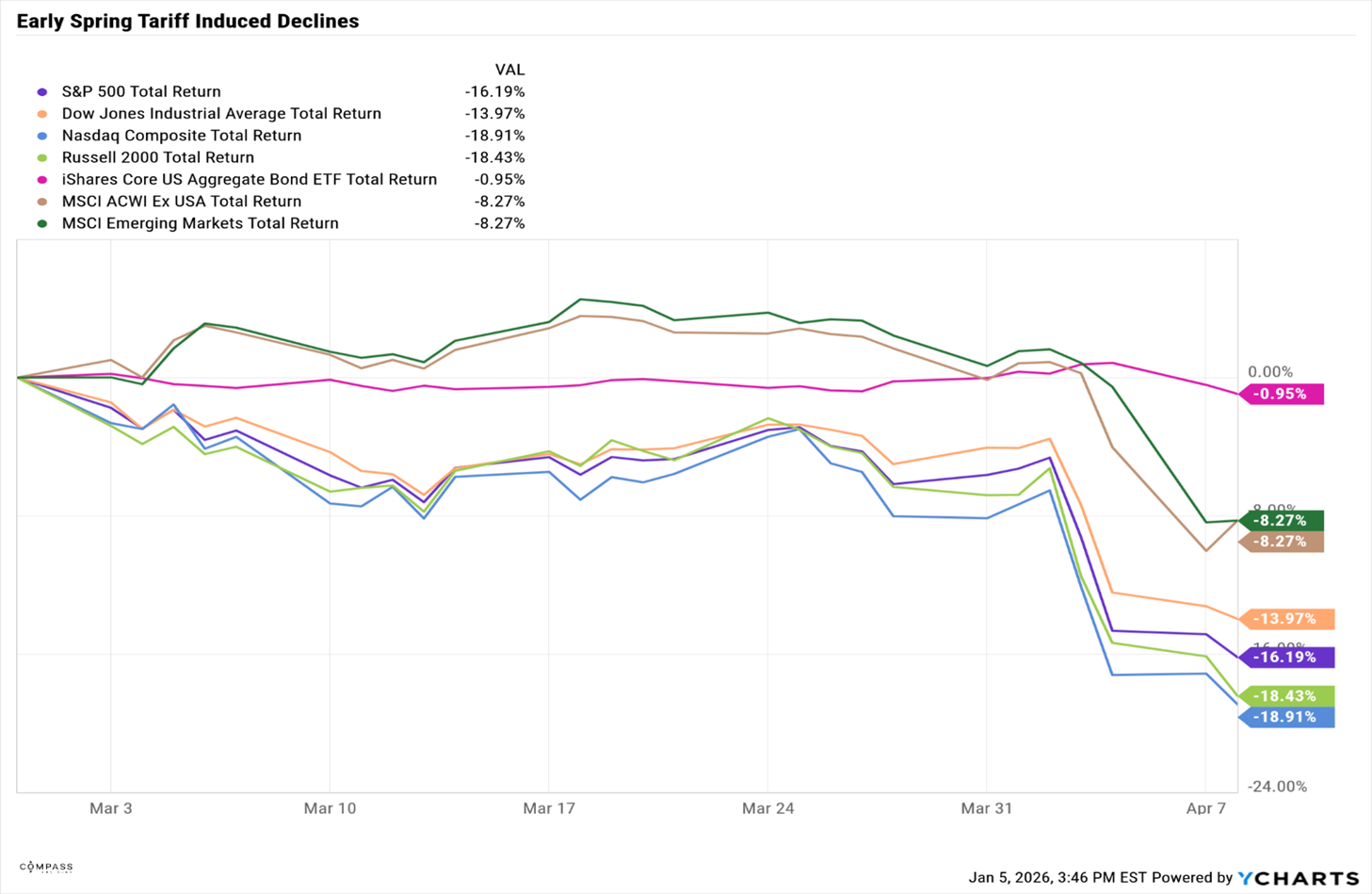

Policy turbulence was the year's persistent background noise. The combination of higher tariffs and accelerating technology adoption effectively reshaped parts of the U.S. economy by channeling capital toward AI, automation, and domestic manufacturing while squeezing trade-exposed industries and some consumer-facing businesses. The geopolitical fears took its toll on the market early in the year with an early Spring decline that approached 20% in the S&P 500 and the Nasdaq.

Key Themes and Takeaways for 2025

The U.S. avoided recession and grew at a solid 2% pace, though the gains were not felt equally. Recent research reveals that roughly 60% of GDP growth is being driven by the AI buildout.

While technology thrived, manufacturing struggled and wage growth cooled, highlighting both the economy's underlying strength and the uneven nature of this expansion.

Consumer prices moved closer to the Fed's comfort zone, settling into the high 2% range by December. However, the final stretch proved bumpy as tariff-related pressures and persistent housing costs complicated the path.

The Federal Reserve responded with three rate cuts, moving away from its most restrictive stance while signaling that future cuts would be measured and deliberate.

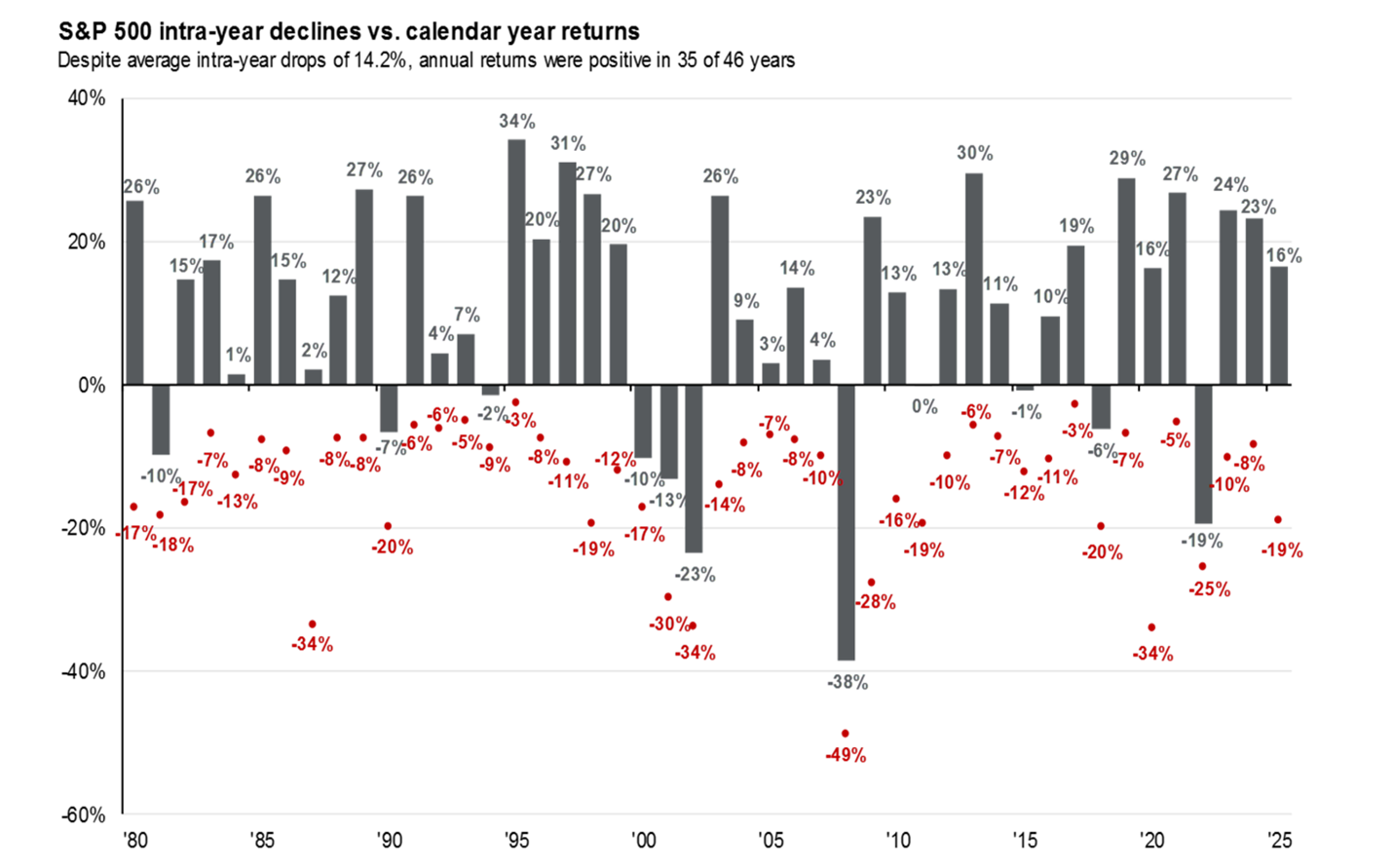

For long-term investors, last year demonstrated that markets can move forward even when headlines feel uncertain. Despite political turbulence and a cooling labor market, positive earnings growth and moderating inflation provided the foundation for another year of gains. Below is a favorite chart that shows the calendar year return of the S&P 500 since 1980 along with the intra-year decline that took place in each year. It is a powerful reminder that downside volatility is normal throughout the year, and even when double digit declines take place, it does not mean the year won’t be a positive one.

Looking Ahead in 2026

We believe that an accommodative Federal Reserve Policy that gradually continues to lower rates puts wind in the sails of the stock and bond markets. This can drive bond prices higher and boost business spending at more reasonable borrowing costs. If earnings can continue to deliver on expectations, markets can continue to thrive as they have over the last 3 years. We will continue to balance the risk reward tradeoffs for client portfolios and adapt to changing conditions and policies.