2025 4th Quarter investment bulletin

Executive Summary

Stock gains continued higher in the 3rd quarter led by technology. With the "Magnificent 7" accounting for 35% of the S&P 500, stretched valuations become a concern.

The bond market benefited from declining interest rates as the Fed lowered benchmark rates by 0.25%.

The economic outlook appears strong as GDP growth accelerated in the 3rd quarter led by the American consumer.

Uncertainty over tariffs, persistent inflation and historically high stock valuations are potential headwinds going into year-end and 2026.

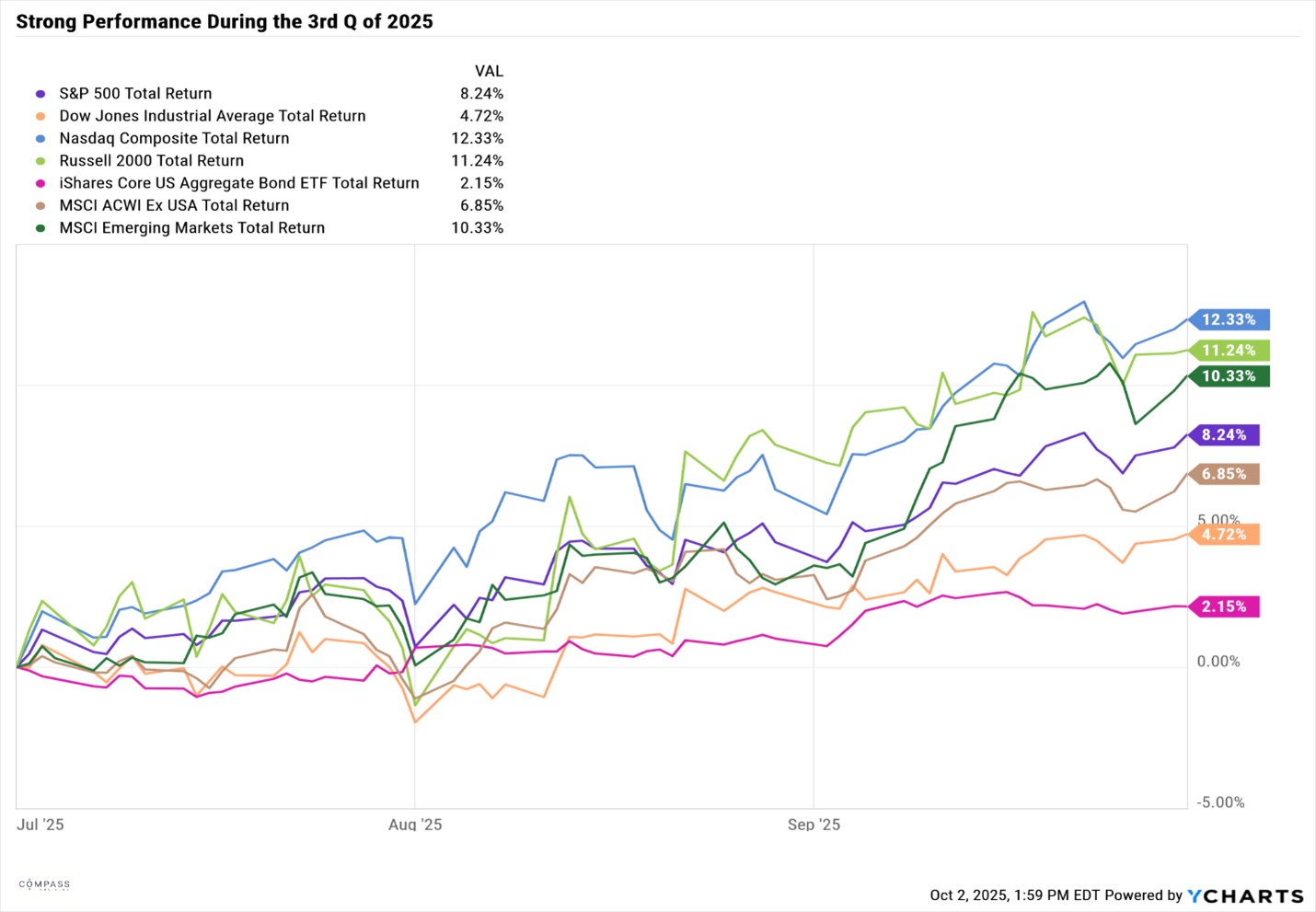

Major U.S. Stock Indicies

AI technology and the "Magnificent 7" powered returns in the 3rd quarter, however the gains expanded to other areas of the market with Small/Mid Cap Stocks and Emerging Markets also posting strong performance.

Key Themes in the US Economy

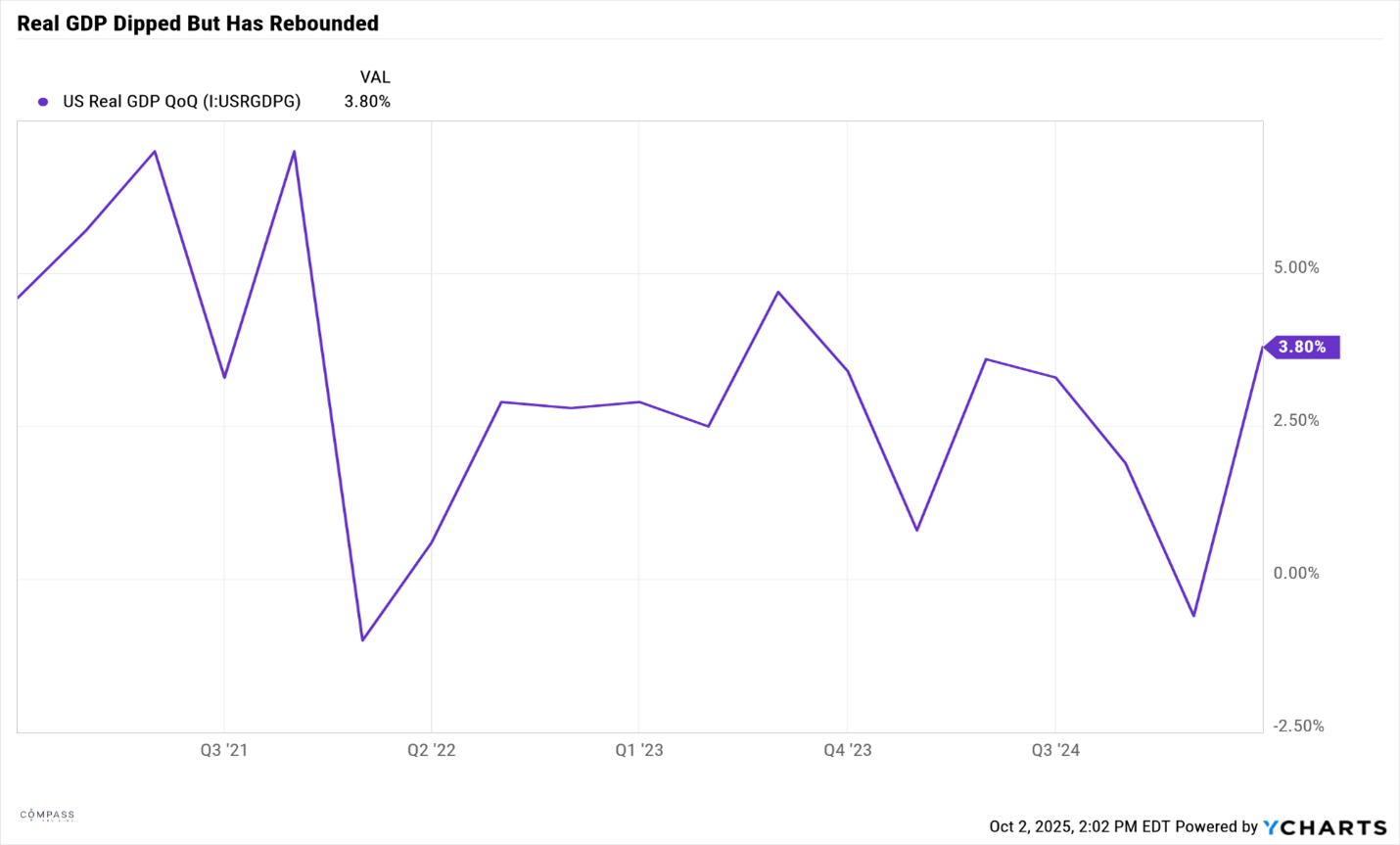

GDP:

Gross Domestic Product (GDP) is the primary indicator for the health of the U.S. economy and posted a significant rebound from Q2-2025. This turnaround was predominantly driven by the strong and persistent American Consumer as well as a spike in net exports.

Tariffs:

Strong economic data and moderating inflation allowed the Federal Reserve to lower key benchmark rates in September by 0.25%. However, the potential inflationary impact of tariffs and unpredictability of U.S. foreign trade policy are causes for investor concern and pose a challenge for future rate cuts.

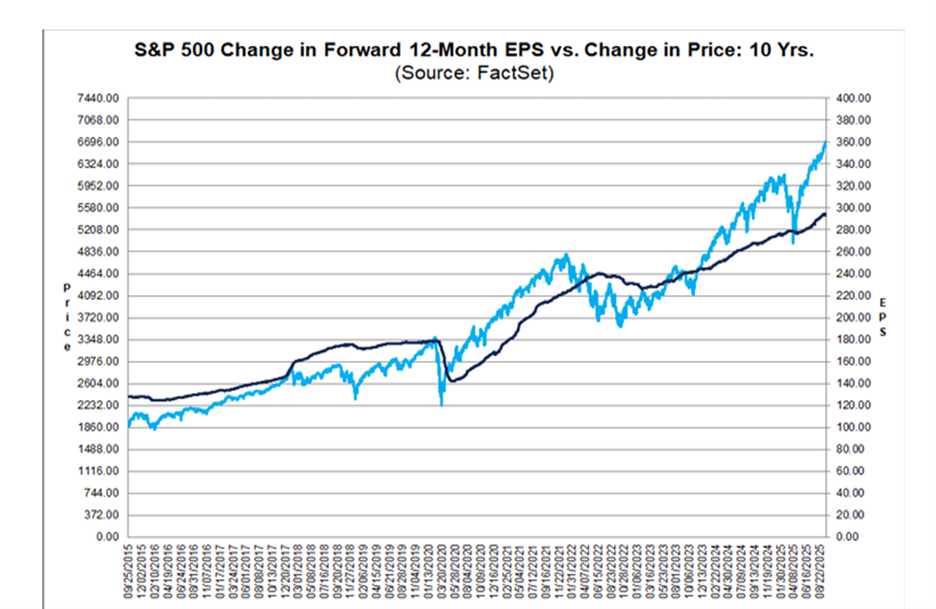

Current Market Valuations:

Technology stocks continue to be the primary driver of market returns and the “Magnificent 7” now represent 35% of the S&P 500 market cap and 45% of its performance. This expansion has led to historically high valuations relative to earnings. As the chart below indicates, the gap between market price and company earnings is historically wide. In order for this disparity to moderate and come into equilibrium, stock prices will need to fall, earnings rise, or some combination.

Current Outlook & Positioning

From a portfolio positioning standpoint, it is critical to remain broadly diversified as the market becomes materially more concentrated. This is achieved by the continued allocation to asset classes and sectors other than large-cap growth. For example, a continued allocation to small-cap stocks proved detrimental in the first two quarters of 2025 but was helpful in the 3rd quarter. Historically, when the Nasdaq crashed in the 2000 to 2002 period, allocations to small-cap and value provided much needed support during an incredibly challenging time for the high-flying technology sector.