2019 1st Quarter Investment Bulletin

After a turbulent end to 2018 seeing the S&P 500 decline over 14% in the 4th Quarter, markets have recovered meaningfully in the early part of 2019. And while we continue to be optimistic about the near-term economy, we are growing cautious about risks to portfolios given the almost 10-year bull market for US Equities.

We have begun the rebalancing process for clients over the past few days. The trades are designed to accomplish two primary goals. First, we are strategically reducing stock allocations by approximately 5-10% across accounts. Second, we continue to seek out investments that are diversified and low-cost.

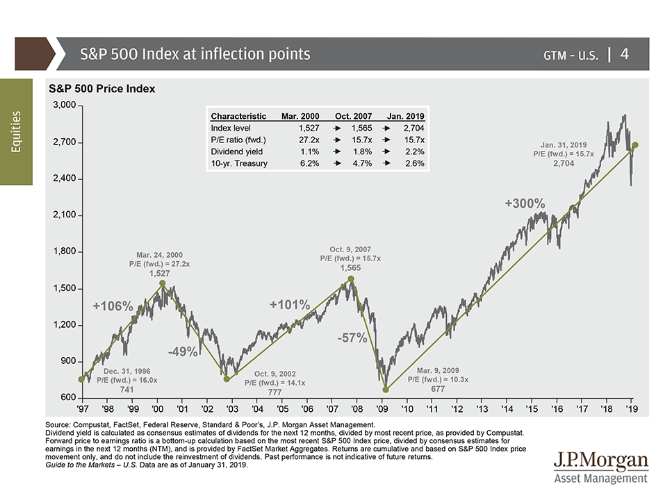

The reason for the more cautious posture in portfolios is a direct result of the incredible bull market that we’ve had the fortune of participating in during the last decade. The chart below, which shows the S&P 500 at inflection points during the last twenty years, makes a compelling visual case that more cautiousness may be in order soon. The pattern that is depicted is one in which large gains have been followed by very large losses. While we don’t believe we are able to time the short term ups and downs of the stock market, we do believe that the current valuation lends itself to being more defensive.

The 4th quarter of 2018 reacquainted most investors with deeper portfolio losses. After reaching all-time highs in September, the U.S. stock market proceeded to decline more than 14% during the last three months of 2018. As swiftly as losses mounted during the 4th quarter, the stock market bounced up 8.5% during January. This recovery in value gave us a greater sense of comfort in moving to a more cautious posture.

The incremental reduction in stocks will not be a large hindrance to your portfolio should the gains continue, but will be a moderating factor should losses resume. Further, we believe it is prudent to have a plan of action to opportunistically take advantage of market losses should they materialize. In the event of a market correction, we will look to add exposure to stocks at more attractive valuations.